The capital markets have suffered a “crude” awakening in March 2026. In this post, we share why pre-IPO planning is the single highest-leverage investment emerging growth companies and their sponsors can make (regardless of which liquidity path they ultimately pursue).

Key Takeaways: Hope is not a Management Strategy

- Pre-IPO planning is not a bet on going public. It is the best way to preserve the greatest number of liquidity options and maximize the value of whichever option you ultimately pursue whether that be IPO, M&A, secondary sale, dividend recapitalization, or otherwise.

- Lack of planning makes everything else harder. Buyers discount unprepared businesses. Bankers cannot move quickly with messy cap tables and unaudited financials. Windows close before you can act.

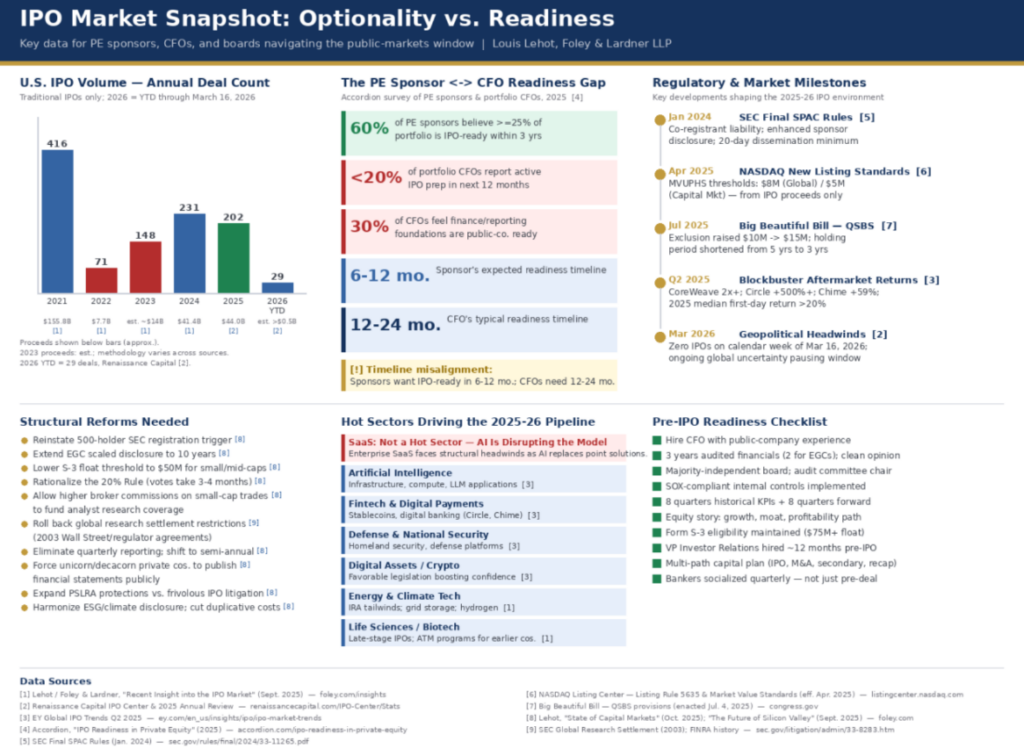

- Accordion’s 2026 survey reveals the scale of the problem: 60% of PE sponsors see IPO potential in their portfolio within three years, yet fewer than 20% of portfolio CFOs are actively preparing. Only 30% feel their finance and reporting foundations are fully public-company ready.

- The regulatory environment has added new complexity: SEC SPAC rules, updated NASDAQ listing standards, and the QSBS overhaul in the Big Beautiful Bill all reshape the landscape for boards thinking about exits.

- Our counsel after 25 years in these trenches: optionality beats perfection, liquidity beats price, and readiness beats hope. The companies that achieve the best outcomes are not the ones that started preparing when the window opened. They never stopped.

There is a question we hear constantly from boards and management teams of PE-backed companies: “Should we start thinking about IPO readiness?” Our answer is always the same, and it surprises some of them. The question is wrong.

Pre-IPO planning is not (or should not be) a decision you make when you decide to go public. It is the foundational work that gives a company the greatest possible chance of achieving the best possible liquidity outcome, whatever that outcome turns out to be. An IPO-ready company is a better M&A target, commands better terms in a secondary sale, qualifies more cleanly for a dividend recapitalization, and has more leverage with lenders and strategic partners across the board. Pre-IPO planning does not narrow your options. It multiplies them. Not doing it does the opposite.

The IPO market of 2025 and early 2026 makes this point vividly. After a four-year high in 2025 where 226 IPOs raised $43 billion, with blockbuster aftermarket returns from CoreWeave, Circle, and Chime, the floodgates were set to open in 2026. But a “crude” awakening has since slammed the window shut. As we write in mid-March, 2026, there are zero IPOs scheduled for the current week. Geopolitical volatility has rattled markets and paused a pipeline that looked robust just months ago. Companies that had been preparing for years are positioned to move the moment conditions stabilize. Companies that had been waiting for the right moment to start preparing are not.

The Gap Is Bigger Than Anyone Wants to Admit

A 2026 Accordion survey of PE sponsors and portfolio company CFOs quantifies a readiness gap that many in the market feel, but few discuss directly. Sixty percent of sponsors believe at least a quarter of their portfolio companies could be prime IPO candidates within three years. But fewer than 20% of those companies’ CFOs report any active IPO preparation underway in the next 12 months. Only 30% feel their finance and reporting foundations are fully public-company ready.

The timeline disconnect is equally stark. Sponsors that are sitting on aging assets with LP pressure building expect portfolio companies to achieve IPO readiness in six to 12 months. CFOs, who must actually implement the transformation, know it realistically requires 12 to 24 months. This is not a small misalignment. It is a structural gap that, unaddressed, will cost sponsors real value when the window opens, and they cannot move.

What created the gap? The IPO market was largely closed from 2022 to 2023. Companies that would have been going public instead pivoted to survival mode: cutting costs, managing debt, and pursuing private financing alternatives. IPO readiness was deprioritized because the market wasn’t going to reward it. That was a rational short-term choice. The long-term cost is that many companies now lack the financial infrastructure, governance structures, and institutional-grade reporting that any sophisticated exit requires (not just a public offering).

Readiness Is the Answer — Whatever the Question

Here is what we tell every board we work with: the question of whether to pursue an IPO is secondary. The primary question is whether your company is the kind of company that can pursue an IPO, because that same state of readiness is what drives the best outcome in every other scenario too.

In an M&A process, a company with two years of clean, audited financials, SOX-compliant internal controls, a majority-independent board, and a well-documented equity story commands a materially better valuation and a faster, lower-friction process than one that does not. Buyers price unprepared businesses at a discount. This is not because of what they find, but because of what they cannot verify. Every week of additional due diligence is leverage in the wrong direction.

In a secondary sale, institutional buyers (e.g., growth equity funds, sovereign wealth vehicles, crossover investors) apply the same scrutiny as a public market investor. They want historical KPIs, forward projections with eight-quarter visibility, a clean cap table, and a management team that understands its own numbers well enough to defend them. A company that has been doing pre-IPO planning has all of this. A company that has not is improvising under pressure.

In a dividend recapitalization, lenders need confidence in the stability and predictability of cash flows. That confidence is built on exactly the same financial reporting discipline and governance infrastructure that IPO readiness requires. And in a strategic partnership or licensing arrangement, the credibility that comes from institutional-grade disclosure and governance is often the difference between a deal that closes and one that does not.

The point is not that every company should go public. Many companies, particularly those with more than $100 million in revenue growing at strong rates with healthy gross margins, have ample private capital available and no compelling reason to absorb the cost and scrutiny of a public listing. The point is that the preparation required to have the IPO as a genuine option is also the preparation that makes every other option better. Pre-IPO planning is not a path. It is a platform.